Pakistan is currently traversing the most critical existential nexus in its history, teetering on the edge of a growth crash and chronic stagflation. The state stands at the brink of sovereign collapse, pushed by the confluence of a long-term hybrid rentier-elite capture model, a persistent security-first paradigm, and the acute 2026 “Hormuz Shock”. This crisis has manifested as a profound societal breakdown, with Inflation (CPI – Consumer Price Index) driven by an almost 222% surge in diesel prices and spiraling electricity tariffs required to manage a bloated circular debt. The current “firefighting” approach—raising prices to meet IMF (International Monetary Fund) demands while protecting elite interests—is fundamentally unsustainable. A radical strategic pivot is now required to transition Pakistan from an extraction state into a productive, export-led growth model.

The Historical Divergence

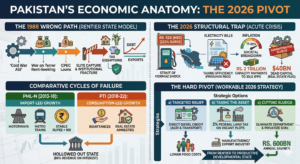

The “wrong path” was cemented in the late 1980s. While regional peers like China, Singapore, Vietnam, and South Korea embraced global supply chains and strict performance discipline, Pakistan doubled down on geostrategy rent-seeking. By leveraging its location to secure aid and loans, the state created a moral hazard where structural reforms were perpetually delayed by the hope of the next bailout.

This era also solidified an institutional fracture where the political and bureaucratic elite prioritized short-term survival through patronage and untaxed real estate over long-term national prosperity. Consequently, an undocumented economy flourished, with 40-70% of GDP remaining informal. This ensures that the tax collection burden falls disproportionately on productive industries and the middle class through indirect taxation on energy and fuel, failing to address the underlying fiscal deficit.

The 2026 Acute Crisis and Strategic Misalignment

The government’s response to the current energy and inflation crisis is characterized by strategic misalignment. In the petroleum sector, the policy of full price pass-through to satisfy IMF programs, combined with a high petroleum levy, has collided with regional strikes that severed the Gulf lifeline. As a result, diesel prices have surged by 222% due to refined product scarcity. This functions as a “tax on the poor”; while subsidizing motorbikes is a popular political move, it fails to solve the broader collapse of agricultural transport and commodity operations.

Similarly, the electricity sector is witnessing “grid cannibalization”. New prosumer regulations for 2026 discourage rooftop solar by switching from net metering to net billing, effectively taxing efficiency to pay for dead assets. Subsidies have been stripped away as grid tariffs hit Rs. 50-70 per unit, driven largely by Rs. 2.1 trillion in capacity payments to idle Independent Power Producers (IPPs) under rigid “take-or-pay” contracts. With CPI remaining in the 17-20% range, the middle class is being crushed to pay off state debt.

A Legacy of Failure

This consistent failure stems from two flawed versions of the same extraction model. The consecutive governments may it be under Military ruler of elected have focused on import-led growth via massive infrastructure projects like CPEC. They artificially defended the exchange rate to the dollar, which provided a temporary sense of rupee stability but led to foreign debt account deficit and a balance of payments crisis. Governments also relied on consumption and remittances. By delaying the IMF program and introducing unsustainable real estate amnesties, they diverted vital capital away from the industrial sector. The shared failure of all these models is evident today: by 2026, external debt servicing and interest rates consume 80% of federal net revenue, leaving the state hollowed out.

Institutional Roadblocks: Sludge and Elite Immunity

The path to reform is blocked by “administrative sludge”—the regulatory friction that PIDE estimates will cost the economy over $142 billion in potential welfare gains by 2030. This sludge is deliberately maintained to shield elite immunity, forcing capital to remain in the frictionless, informal real estate “file” culture.

Currently, tax collection via the FBR fails to capture “dead capital”—the $40 billion parked in untaxed real estate files and the protected retail sector. Furthermore, the compound effect of military interventions has created a state strong in security but weak in service, where military-led business create a crowding-out effect that stifles private investment.

The Hard Pivot: Workable Options for 2026

To break this cycle, the government must execute a “hard pivot” toward geoeconomics. First, immediate relief must be provided through an “Agri-Shield”. Instead of blanket subsidies, the state should use digital IDs to provide direct diesel credits solely for agricultural tube-wells and food transport, lowering food prices without favoring car owners.

Second, the tax collection model must shift from income to assets. Implementing a mandatory 2% national wealth tax on vacant urban plots would make it more expensive to hold a “file” than to build a factory, forcing capital into the formal manufacturing sector and boosting exports. Third, the state must perform a “sludge audit,” eliminating 30+ redundant regulatory bodies to save approximately Rs. 600 billion annually and privatizing chronic loss-making enterprises, which they have already started.

Finally, an energy structural redemption is required. By converting the Rs. 2.1 trillion capacity payment liability into long-term sovereign bonds, the government can lower the immediate burden of debt repayment on monthly bills. This is the only real path to incentivizing industrial consumption and earning the foreign exchange needed to solve the larger balance of payments crisis.

Conclusion

Pakistan’s failure is not due to a lack of a model, but a lack of institutional will to implement one. The current path is a choice, not a destiny. The lesson from East Asian export-led growth is clear: security follows the economy, not the other way around. The only viable option for survival is to tax dead assets and lower energy costs for industry, creating a productive developmental state.

End Notes

PIDE (Pakistan Institute of Development Economics). (2024). The Elite Capture of Pakistan’s Economy: A Diagnosis.

Husain, K. (2026, April 3). The Hormuz Shock: Severed Supply Lines and the Petrol Bomb. Dawn.com.

Husain, I. (2018). Pakistan: The Economy of an Elitist State. Oxford University Press.

Amsden, A. H. (1989). Asia’s Next Giant: South Korea and Late Industrialization. Oxford University Press.

Zia, A. (2025). Moral Hazard and the IMF Cycle: Pakistan’s Perpetual Bailout.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics, 3(4), 305-360.

PIDE. (2025). Mapping the Shadow: Estimates of Pakistan’s Informal Economy.

IMF (International Monetary Fund). (2024). Pakistan: Third Review Under the Stand-By Arrangement.

NEPRA (National Electric Power Regulatory Authority). (2026). Review of Distributed Generation (Net Metering) Regulations.

State Bank of Pakistan (SBP). (2018). Annual Report on the State of Pakistan’s Economy.

Rana, S. (2022). Delay in IMF Program Cost Pakistan $10bn. The Express Tribune.

PIDE. (2024). The Cost of Sludge: Regulatory Impediments to Business in Pakistan.

Siddiqa, A. (2007). Military Inc.: Inside Pakistan’s Military Economy. Pluto Press.

Husain, K. (2026, April 12). Motorbike Subsidy: A Political Band-Aid on a Structural Wound. Dawn.com.

Studwell, J. (2013). How Asia Works: Success and Failure in the World’s Most Dynamic Region. Grove Press.

Ministry of Finance, Government of Pakistan. (2025). Annual Report on State-Owned Enterprises (SOEs).

IMF. (2025). Pakistan: Technical Assistance Report on Circular Debt and Energy Sector Reforms.