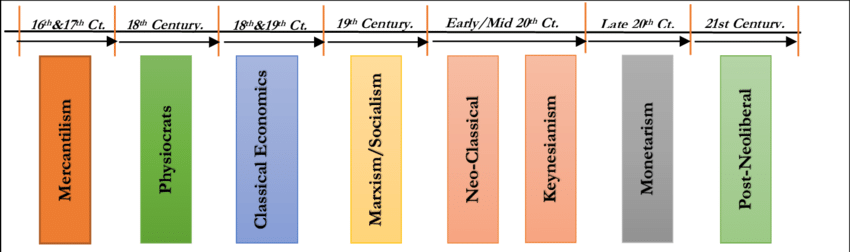

The Eternal Debate: The Market and the State

In the bustling city of Economica, two powerful forces have long vied for control over the lives of its citizens: the Market, a vibrant, chaotic spirit born from the collective pursuits of millions of individuals, and the State, a towering guardian who believes order must sometimes be imposed from above. Their rivalry shapes the prosperity, crises, and destinies of the people. Over centuries, great sages have emerged, each championing one side or seeking a delicate balance, as the city evolves through booms, busts, and revolutions.

It began in the 18th century with the sage Adam Smith, who gazed upon the city’s workshops and trades.

He saw beauty in the chaos. “Picture our economy as a massive machine that runs best when left alone,” he declared. The Market, he said, possesses an Invisible Hand—millions pursuing their own self-interest unknowingly create order. A baker bakes not to feed society, but for profit—yet bread appears on every table. Prices and wages adjust naturally: too much bread, prices fall; too few workers, wages rise. With allies like David Ricardo, who preached comparative advantage—nations thriving by specializing—these classical voices warned the State: “Interfere, and you throw a wrench into the gears. Laissez-faire—let it be!”

The Market cheered, flexing its freedom as trade flourished. But in the smoky factories of the Industrial Revolution, shadows grew.

There rose Karl Marx, a fiery prophet who saw not harmony, but a battlefield.

“The Market is exploitation disguised as freedom,” he thundered. Value comes from labor alone: a worker crafts chairs worth hundreds, yet receives pennies while the owner pockets the surplus. This inevitable contradiction, driven by historical forces, would build pressure until capitalism exploded into revolution, birthing socialism and communism. The State, in Marx’s vision, must seize the reins to liberate the workers.

The city trembled as class wars erupted, with the Market accused of devouring the weak.

Yet not all saw pure conflict. In quiet studies, thinkers like John von Neumann and John Nash viewed the struggle as a grand chess game.

Game theory revealed the Prisoner’s Dilemma: rational self-interest often leads to mutual ruin, like firms in price wars or nations in arms races. Nash equilibria emerge—everyone driving on the same side of the road, not because it’s best, but because deviation is disastrous. Here, neither pure Market nor State dominates; outcomes depend on anticipating others’ moves.

As the 19th century waned, neoclassicals refined the Market’s defense, focusing on individual choices and marginal utility—why diamonds sparkle dearer than water. They dreamed of perfect competition, with supply and demand in eternal equilibrium.

But then came catastrophe: the Great Depression, when the Market’s machine ground to a halt.

Breadlines snaked through streets as fear paralyzed spending. Into this despair stepped John Maynard Keynes.

“The Invisible Hand needs a push,” he argued. When private demand falters, collective thrift becomes poison. The State must spend boldly—build bridges, hire workers—igniting a multiplier that revives the flow. For the first time, the State was hailed as savior, not saboteur.

The city recovered, but inflation soon raged in the 1970s. Milton Friedman countered with monetarism.

“Inflation is always a monetary phenomenon—too much money chasing too few goods.” Blaming the State’s meddling, he urged steady money growth and letting markets clear a natural unemployment rate.

Meanwhile, supply-siders like those behind the Laffer Curve whispered to leaders: cut taxes on the productive, unleash investment, and revenue will trickle down.

Booms followed, but so did deficits and inequality debates.

Beyond Economica’s borders, development sages pondered why some lands prospered while others languished in poverty traps. Institutions—laws, rights, governance—proved key, neither pure Market nor overbearing State sufficing alone.

Austrians like Hayek decried central planning’s hubris: no State can match the Market’s spontaneous order via prices. Behavioral economists exposed human irrationality, suggesting gentle nudges. New Institutionalists highlighted transaction costs and path dependence. Public Choice theorists warned that the State, too, is driven by self-interest—politicians chasing votes, leading to captured regulations.

And so the story continues in Economica today. The Market pulses with innovation and freedom, yet falters without guardrails. The State offers stability and justice, yet risks overreach and stagnation. No single sage has won the debate; each era calls forth a new balance, as citizens navigate the eternal tension between individual pursuit and collective good. In this grand tale, prosperity emerges not from triumph of one over the other, but from their uneasy, ever-shifting dance.